Standalone Financial Advice

If a client wishes for Baron & Grant to manage their portfolio, the FCA stipulates we need to provide one-off ‘gateway’ financial advice to determine the most suitable portfolio, for which we charge £750. This fee represents 0.3% of our minimum investment of £250,000.

Full Financial Planning & Advice

Should clients require wide-ranging financial advice, one of our qualified financial advisers can help cater for an extensive range of personal requirements – from protecting a client’s family, pension and estate planning, to passing on wealth to chosen beneficiaries.

| Band | Initial Charge | Charge for Full Band |

|---|

| £0 to £500,000 | 2.0% | £10,000 |

| £500,000 to £1m | 1.0% | £5,000 |

| £1m+ | 0.0% | Nil |

Ongoing Advice Service (Optional) – To ensure ongoing suitability of your advice throughout your financial journey. Our ongoing advice fee is 0.5% of funds under management.

Discretionary Investment Management

Our investment team manage investment trust focused portfolios which are complemented by a carefully selected range of exchange-traded funds (ETFs).

This approach is different to the vast majority of investment or wealth managers who run portfolios consisting in large part of direct equities and/or other forms of collective funds such as unit trusts and open-ended investment companies (OEICS). Such funds on average have been shown to underperform investment trusts.

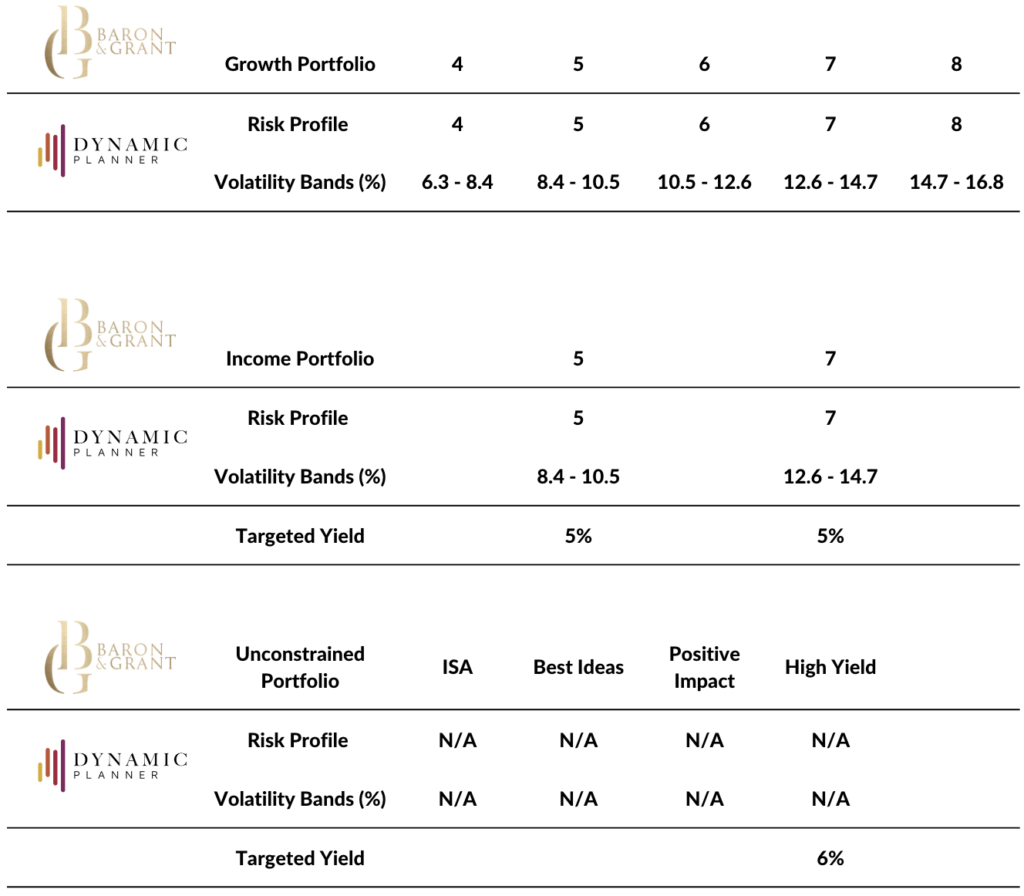

We offer a range of eleven model portfolios which span the full spectrum of risk-adjusted returns, thus enabling us to fully accommodate our clients’ different investment objectives and profiles.

Seven portfolios are categorised by Dynamic Planner Profiles 4 to 8 – the risk/reward remit increasing with the profiles. Five portfolios (B&G 4, 5, 6, 7, and 8) are focused on capital growth, while two are income-orientated, aligned to risk profiles 5 and 7, with a targeted yield in excess of 5%. We also offer four unconstrained portfolios – Positive Impact, ISA, High Yield (with a targeted yield in excess of 6%) and Best Ideas.

The major element of each portfolio consists of proven and respected investment trusts, which are then complemented by a carefully-selected number of ETFs. We are fortunate in that there is a vast array of different investment options from which to construct our portfolios.

We continually monitor the portfolios to ensure an optimum balance between remit and risk. The investment committee formally meets once a month and portfolio changes are undertaken quarterly, or whenever required.

By providing financial planning, advice and discretionary investment management in-house, clients benefit from a cohesive approach to their wealth management.

Our discretionary investment management fee is 1% per annum, payable monthly in arrears.

The minimum investment for this service is £250,000.

Download Client Brochure

Third Parties

The FCA rightly requires the disclosure of all costs – our own and the third parties we use.

Annual platform charge

B&G do not hold client cash or assets. Client investments are managed on what is known as an investment/wrap platform. Our chosen platform partners are:

- AJ Bell Investcentre

- M&G Wealth Platform

- Transact

- 7IM

- Nucleus

- Wealthtime (formerly Novia)

- Fundment

Our chosen platform partners provide B&G with on-line dealing, valuation and custody services. Clients have the ability to login and access their portfolio valuation(s) at any time.

Each platform partner has its own charging structure, however annual platform charges tend to start around 0.25% of the portfolio value. This charge tiers down for higher portfolio values and family linking facilities are available (platform dependent). Charges are deducted monthly in arrears and are calculated in relation to a daily valuation.

A detailed breakdown of the recommended platform costs and charges will be provided as part of our advice process.

There are many benefits associated with investment/wrap platforms. These include:

- Institutional dealing capability with no dealing fees (platform dependent)

- Ability to consolidate existing products and policies onto one platform for ease of administration

- Ability to rebalance portfolios to keep them in line with desired risk profile – this is difficult and often costly to achieve on DIY platforms

- Access to up to date portfolio valuations online 24/7

- Consolidated reporting enabling accurate and efficient calculation of CGT liability (provided all chargeable assets are administered on the platform)

Personal Finance Portal (PFP)

Personal Finance Portal (PFP) is a service available only from a financial adviser. We use the portal to gather personal and financial information to try and ensure an efficient onboarding process. It also provides B&G with:

- Secure encrypted messaging

- Secure encrypted Document Vault – store financial documents online securely and fully backed up

- Access to Open Banking – a service that enables you to collate information from bank accounts and credit cards, giving you powerful insights

The underlying investments – OCF (Ongoing Charges Figure)

Investment trust costs are expenses that impact the Net Asset Value (NAV) rather than being deducted from the investor’s capital. Investors discount these recurring expenses in the share price.

In late 2024, the FCA introduced a MiFID and PRIIPs exemption, meaning investment trust costs no longer need to be aggregated into the total cost figures of portfolios that hold them. This was enacted through legislation and the FCA Handbook via COBS 6.1ZA.14 and 14.3A.11.

As a result, the single aggregated ongoing charges figure (OCF) of our portfolios reflects only the weighted cost of ETFs held — typically 0.03% to 0.1%. Some of our unconstrained portfolios contain solely investment trusts and therefore have an OCF of zero.

Many platforms and data providers have yet to reflect this regulatory change. You may receive Annual Costs and Charges statements that quote an erroneous investment product cost, which you are not actually paying. If you require any clarification on this matter, please contact us.

Security of assets

B&G have carried out extensive due diligence on our platform partners to ensure financial strength, resilience, stability, ongoing investment, functionality and competitive fee structures.

Your cash and assets are held separately from their accounts and from those with whom they place the assets. As such, should a platform be wound up, your cash and assets will remain yours and any administrator is obliged to return them to you as part of the wind down process.

Clients also have access to the Financial Services Compensation Scheme (FSCS) for qualifying investments and cash – subject to the limits.

Please find each platform’s security of assets literature below:

M&G Wealth – Security of Assets

AJ Bell Investcentre – Security of Assets

7IM – Security of Assets

Further detail on the security of assets for the respective platforms can be provided upon request.

B&G is an independent, owner managed business which was established in 2019. B&G does not carry any debt and has a strong balance sheet and liquidity position. The UK Investment Firms Prudential Regime (IFPR) came into force on 1st January 2022 and B&G is classed as a MIFIDPRU Investment Firm. As a MIFIDPRU investment firm, B&G’s own funds requirements will be the highest of:

- Its Permanent Minimum Capital Requirement (PMR) of £75,000

- A Fixed Overheads Requirement (FOR) of 3 months fixed costs

The FCA expects firms to assess at least annually, the full financial resource requirements in relation to specific risks that a firm faces.

As a firm that falls within scope of the IFPR, B&G has submitted its Internal Capital Adequacy and Risk Assessment (ICARA) to the FCA.

Based on the firm’s unaudited financial accounts for the year ended 31st December 2025, B&G had more than 8.9 times its FCA own funds requirements.

Our compliance consultants are threesixty Services LLP. Threesixty delivers support and compliance services to over 950 directly regulated IFA practices, including over 100 discretionary investment management firms, equating to over 10,000 registered individuals. Their experts provide an unparalleled understanding of the issues impacting discretionary management firms, and their service ensures our in-house compliance resource gets the help, expertise and external opinion it needs.

With regards to our track record, whilst we have only been authorised since the 4th January 2021, we can point to the track record of John Baron’s actual real investment trust portfolios (‘Growth’ and ‘Income’) in his popular monthly column in the Investors’ Chronicle magazine. John has reported on these portfolios monthly, trade by trade, since the 1st January 2009. These are two of ten actual portfolios that John has managed, which have an auditable track record of performance.

Our portfolios share the same foundation, DNA, style, and themes.