Continue to profit from the great British sell-off

Investors sometimes forget that a country’s economy and its stock market can often move in different directions. That has certainly been the case with the UK market this year, which has outperformed global indices – the FTSE All-Share index having returned 20.5% at time of writing, compared to 14.7% for the MSCI World (£) index. The question is whether this is just a flash in the pan or the start of something more sustained. Certainly, the sceptics are legion while domestic investors have run for the woods. Yet it is often darkest before the dawn. With poor economic sentiment, investment outflows continuing and depressed valuations relative to peers, I suggest investors are underestimating the various tailwinds which will continue to make for outperformance. Once again, this is a contrarian trade – and therein lies the opportunity.

Economies and markets

Some decades ago, there was a sustained period when China’s economy was booming and yet its stock market made little progress. It reminded all that economies and stocks can often move in different circles. And this should not come as a surprise. One largely reflects economic management by a government, the other attempts to value how well companies are performing and their outlook. A critic might say the two are closely interwoven. Yet the UK market is an example where such logic falls short. Around three-quarters of the sales of FTSE 100 companies and half those of the FTSE 250 are sourced from overseas – where prospects can be better. Indeed, many of these companies do little or no business in the UK and yet are often valued at a discount to international peers.

A host of economic concerns have tarred most if not all companies with the same brush. An economic model that places dividends ahead of research and development is a concern. A short-term focus on investment, too much regulation stifling enterprise, governments which cannot rein in spending and which is increasingly crowding out the wealth producing private sector, have conspired to make for a near-£110 billion interest charge just to service the national debt – charges which could instead pay for the annual Defence budget, Justice budget and half the Education budget. The resulting tax-take has been too high and is now the highest for nearly 130 years, while living standards have flatlined for decades. No wonder growth is evasive, and enterprise has been heading for the door.

This is not just a British malaise. With a few well-publicised exceptions, this problem plagues most western economies. However, we have allowed this mismanagement to spill over into stock and market valuations. A regulation of the graveyard approach has certainly adversely impacted the investment trust sector, as previous columns have highlighted. Unnecessarily burdensome regulation which downplays the importance of risk taking has also contributed to the quite dramatic decrease in the number of companies listing on the London Stock Exchange over the last 15 years – often to the benefit of competitors. UK pension schemes have not escaped this doom loop given the extent to which they hold British equities has declined from over 50% of portfolio assets in the mid-1990s to mid-single figures today.

It can only get better!

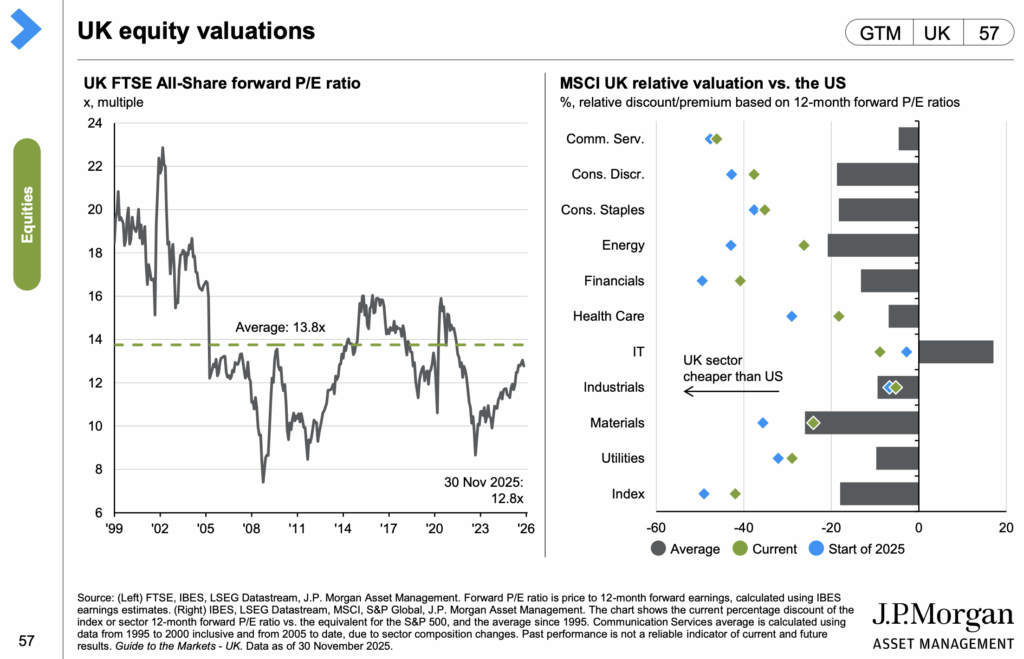

Yet valuations still matter, whatever the focus on AI and the large US technology companies, and reversion to mean remains one of the most valuable investment principles. As the left-hand part of the table from JPMorgan Asset Management shows, despite the UK market enjoying a reasonable run recently, the forward price/earnings ratio remains below its long-term average. And despite a good year (to date!) in relative terms, the market remains on a near-40% discount to the MSCI World index compared to a long-term average of nearly half that number. This in part reflects its composition. The preponderance of commodity, financial and other ‘old economy’ stocks are usually rated at a discount to the more exciting, high-growth technology stocks. Yet I suggest change is in the air.

Relative valuations may be shifting. Markets are still adjusting to a world of stagflation in which growth is poor and inflation is rich – for reasons most recently highlighted in the column ‘Securing value’ (26 September 2025). This tends to favour old economy sectors like banks and mining companies. Banks in part benefit from higher interest rates because they can more readily take a turn between deposits and lending. Commodities usually benefit from higher inflation. This is being given added impetus by current geo-political uncertainties. Previous nuances which have characterised international relations are giving way to hard edges and the realization that certain commodities and metals – including rare earth minerals and precious metals – are more valued pieces on the diplomatic chessboard.

Furthermore, value stocks generally tend to benefit from stagflation. These stocks have been neglected given Quantitative Easing (QE) and artificially low interest rates favoured high-growth stocks because lower discount rates tend to increase the value of future cash flows given the value of money decreases with time. Yet low interest rates have been the exception rather than the rule. The economic environment has now reverted. It is now the era of value stocks once again, in part because of their more reliable near-term cashflows, cheaper ratings and often higher yields.

These are the sort of value stocks which can be found in abundance in the UK – a market the portfolios overweight relative to their MSCI PIMFA benchmarks. Portfolio holdings include well-run investment trusts such as Temple Bar Investment Trust (TMPL), Fidelity Special Values (FSV) and The Mercantile Trust (MRC). Other overseas markets also offer such value, including Europe and many developing markets. As previous columns have highlighted, within their underweighting of equities in general relative to respective benchmarks, the portfolios are positioned accordingly at a cost to the US. Other favoured holdings include Murray International (MYI) and JPMorgan Emerging Markets Income (JEMI).

It is also worth recognising the UK market offers an additional margin of comfort. Poor sentiment can pervade reason beyond good sense. Across a large swathe of market sectors, many not deemed value, UK shares stand on a substantial discount when compared to their US counterparts in the same sector or industry. The right-hand part of the table highlights the current extent and, importantly, the scope for a continued re-rating, given historical ranges. Corporate profitability is certainly higher in the US largely because of their technology stocks, yet these are not typical of the market. Other corporate metrics point to US and UK companies not being too far apart. This further suggests the discount applied to UK companies generally is not rational.

Other straws in the wind suggest existing tailwinds will continue to prevail. The UK is home to sectors which are becoming more valued including defence, after the invasion of Ukraine, and data processing. There are indications that many of our blue chips are stirring from their lethargy and beginning to increase investment and grow, expand overseas and improve profitability. Turnaround stories such as Rolls Royce are not isolated. Meanwhile, Institutional investors are slowly realising the concentration risk posed by their US technology exposure is elevated and are investing more in better value markets, including the UK. News of the commodities’ behemoth Metlen joining the LSE from Athens, and Assura spurning US private equity reminds investors the traffic is not one-way.

Then there is the potential for domestic investors to increase their weightings in UK shares. Figures over the last four years show relentless outflows from equity funds. Sentiment among UK investors has succumbed to economic woe and the deadweight of too much regulation and taxation. Little wonder most ISAs are invested in cash, which is losing money in real terms. More could be done by government to turn this around. The UK’s pension fund industry is the second largest in the world, and yet its exposure to domestic stocks is on average half that of other international pension schemes. Meanwhile, the government should do more to encourage the conversion of cash ISAs into UK equities. Whether pension schemes or individuals, costly tax breaks should not be a one-way street.

Overall, investors should be cheered by the outlook for the UK market and by investing they will also be spreading a little joy. A strong domestic market assists associated professions – financial services, accountancy, insurance and legal. These remain important components of the economy. Profiting from investments and doing the right thing often co-exists – as the Healthcare sector is, once again, about to prove. With that in mind, I wish all readers every joy and happiness over the festive period, and good health and prosperity in the New Year.

Disclaimer: The information contained in this article does not constitute investment advice or a personal recommendation and it is not an invitation or inducement to engage in investment activity. You should seek independent financial advice as to the suitability of any investment decision. Past performance is not a guide to future performance. The value of investment company shares, and the income from them, can fall as well as rise. You may not get back the full amount invested and, in some cases, nothing at all.

Return to News